Photo by martin-dm from Getty Images Signature via Canva.com

In this article:

The path to homeownership involves multiple steps for veteran and military home buyers, especially if they’re interested in using their VA home loan benefit. A basic understanding of the VA home loan process helps buyers prepare financially and move confidently toward a home purchase.

This comprehensive guide explains how VA loans work, who qualifies, and how to successfully navigate the home-buying process from start to finish.

What Is a VA Home Loan?

A VA home loan is a government-backed mortgage program created to help a service member, veteran, or surviving spouse purchase a home. While the loan itself is issued by private lenders such as banks or mortgage companies, The Department of Veterans Affairs guarantees a portion of the loan, usually about 25%.

This guarantee reduces lenders' risk and makes it easier for a homebuyer to secure favorable loan terms. Since its creation in 1944 under the Servicemen’s Readjustment Act, the program has helped millions of veterans and military members achieve affordable homeownership.

Although VA loans are a powerful purchasing tool, a military or veteran home buyer isn’t required to use one. Depending on financial goals and market conditions, other loan options, such as conventional loans, may be a better choice.

VA Loans vs. Conventional Loans

VA loans differ from conventional loans in several key ways, but mostly because they tend to be more affordable. However, a home buyer should still compare options to determine what best fits their financial situation.

VA Loan Origins

The VA home loan program was established to help returning service members transition into civilian life after World War II. The goal was simple: remove barriers to homeownership and provide financial stability for those who served.

Today, the program continues to support military members, veterans, and their families by offering flexible financing options and foreclosure assistance.

Ways VA loans can be utilized:

- Buy a home or a condominium unit in a VA-approved project.

- Build a home.

- Simultaneously purchase and improve a home.

- Improve the property by installing energy-efficient features or making other energy-saving improvements.

- Buy a manufactured home and/or lot.

- Refinance an existing VA-guaranteed or direct loan for a lower interest rate.

- Refinance an existing mortgage loan.

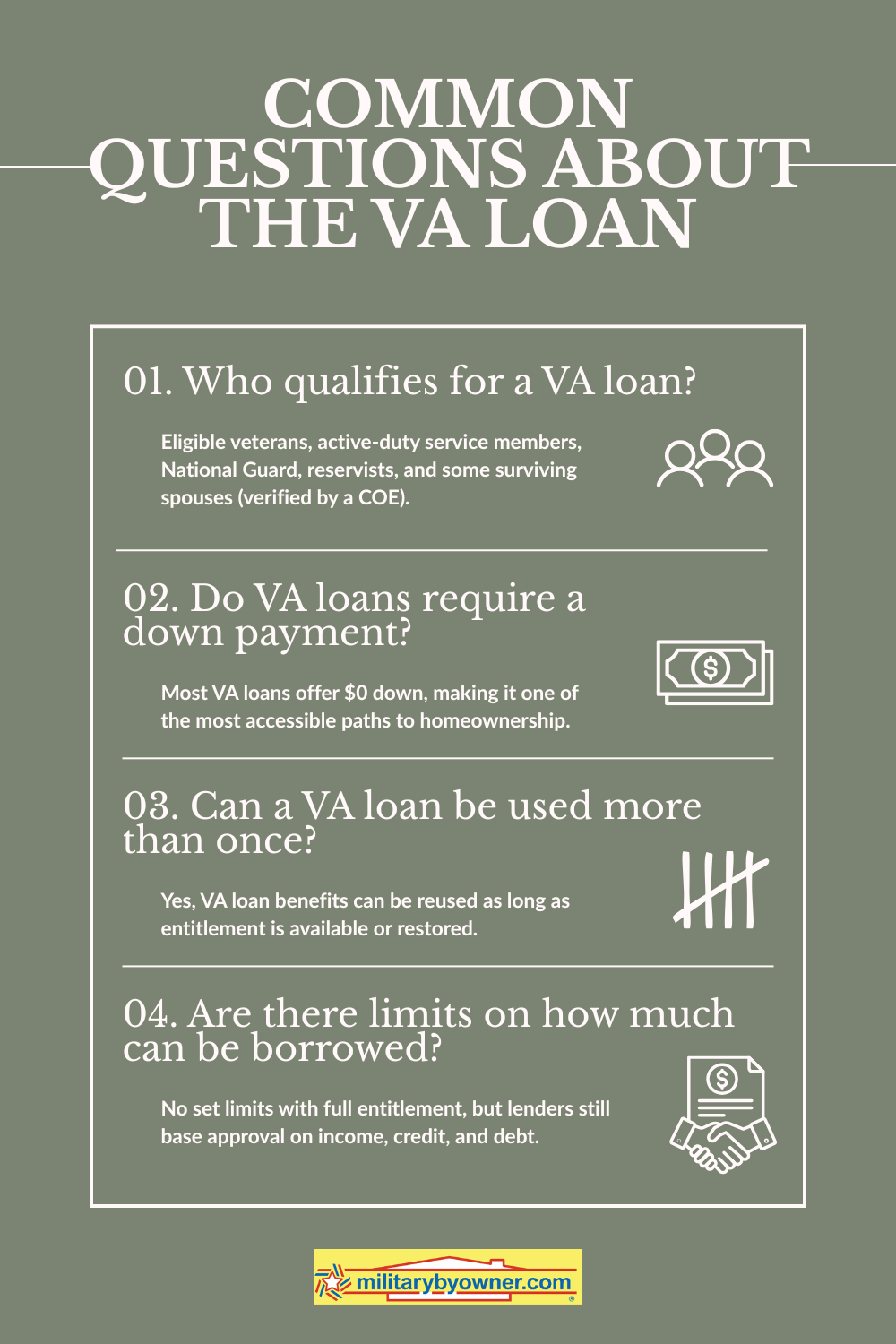

VA Loan Eligibility

Understanding the VA loan eligibility categories is an important first step.

Eligibility is based primarily on:

- Length and type of service

- Duty status (active, veteran, National Guard, or Reserve)

- Type of discharge

Eligible groups typically include:

- Active duty

- Veterans

- National Guard and Reserve

- Some surviving spouses

To verify eligibility, the buyer must obtain a Certificate of Eligibility (COE). Most lenders can quickly access this through the VA’s Loan Guaranty System, although it can also be requested online or by mail if needed.

8 Powerful VA Home Loan Benefits

VA home loan benefits are among the most competitive in the mortgage industry, making them attractive to military families and veterans, especially first-time home buyers.

1. No Down Payment

Qualified borrowers can purchase a home with zero down payment, removing one of the biggest hurdles to homeownership.

2. No Private Mortgage Insurance

Unlike many conventional loans, VA loans don’t require private mortgage insurance (PMI), which can save a homeowner hundreds of dollars each month.

3. Competitive VA Loan Interest Rate

Because the government backs the loan, lenders often offer VA loan interest rates lower than those for conventional loans. Even small rate differences can add up to big long-term savings.

4. Flexible Credit Guidelines

VA loans are more forgiving with credit scores, making them accessible to some buyers who might be shut out of traditional home loans.

5. Limited Closing Costs

The VA restricts certain fees, helping reduce upfront costs.

6. Funding Fee Flexibility

A VA funding fee (usually 0.5% to 3.3% of the total loan amount) helps to keep the lending program afloat, but the fee may be waived for disabled veterans and some surviving spouses.

7. No Prepayment Penalty

A homeowner can pay off the loan early without penalties.

8. Reusable Benefit

A military homeowner can use the VA loan benefit multiple times, even after selling a home or paying off a previous VA loan.

VA Loan Requirements

While VA loans are more flexible than many conventional options, they still require important requirements to be met.

Financial Requirements

- Most lenders look for a credit score of around 580 to 660

- Stable income and ability to repay the loan

- Acceptable debt-to-income ratio

Property Requirements

The house must meet the VA’s Minimum Property Requirements (MPRs), which ensure the property is safe, structurally sound, and suitable for living. A VA appraisal is required to confirm both the home's value and its compliance with these standards.

- The home is a primary residence.

- A multi-family unit (up to a four-plex) is an option if it’s also the primary residence.

- The property must be residential.

- The property must provide enough space for comfortable living, including sleeping, cooking, and sanitary accommodations.

- The electrical and plumbing systems are in good working order and have a reasonable time frame for future use.

- The house has safe and adequate heating systems.

- Safe access from the street is mandatory.

Can you buy a foreclosed home with a VA loan? Get the answers here.

Preparing to Apply for a VA Loan

Even though a VA loan is buyer-friendly, there’s work to be done before the official application process.

Credit Reports

A clean credit report is a must. Months before applying, search multiple credit reports for inaccuracies, small and large, and correct them before applying. The fixes may take a while to appear on a new report.

VA Loan Calculator: Estimating Affordability

A VA loan calculator is a valuable tool for any military home buyer planning a purchase. It helps estimate monthly mortgage payments, interest costs over time, property taxes, insurance, and overall affordability. Using a calculator allows a buyer to set realistic expectations and plan a budget before starting the home search. Find useful calculators at Military.com, Veterans United, or USAA.

Photo by SDI Productions from Getty Images Signature via Canva.com

How to Apply for a VA Loan

The VA loan process can be broken down into the following steps. Understanding each stage helps a home buyer avoid delays and stay prepared.

Explore Pre-Qualification

Buyers might want to investigate an online pre-qualification (different from a pre-approval) to get an idea of their buying power and potential interest rates, but know that this is a surface-level look at finances. A proper preapproval is needed to apply for a VA loan.

Get Pre-Approved

Pre-approval is essential in today’s competitive housing market. A documented approval from a mortgage lender shows sellers that the buyer is serious and financially qualified.

During this step, the lender will:

- Review credit history

- Verify income and employment

- Confirm VA loan eligibility

- Determine borrowing capacity

The home buyer will need to provide documents such as:

- Military ID and driver’s license

- A couple of months of LES statements

- Statement of Service or DD-214

- Pay stubs and W-2s

- Bank statements

- Disability award letters

- Retirement income documents

It’s important not to take on new debt during this stage, because it can affect the loan approval and overall buying power.

Start House Hunting

With pre-approval in hand, the home buyer can begin searching for a home. Working with a real estate agent experienced in VA loans is highly recommended. If house hunting for the first time, ask friends, family, or potential neighbors for recommendations.

Also, check if the agent has a Military Relocation Professional (MRP) designation. It signifies that they’re experienced working with military clients. The agent can help identify properties that meet VA requirements and avoid houses that may fail appraisal due to condition issues.

The Difference Between a Home Appraisal and Inspection

VA loans include protections for the home buyer, such as disappointing appraisal findings. If the appraisal comes in below the purchase price, the buyer may be able to withdraw from the contract without losing earnest money.

Keep in mind that a home inspection is different from a home appraisal. The VA requires an appraisal, but not an inspection. However, most buyers insist on a home inspection to learn about the problems they might inherit. In the most competitive home sale markets, buyers can choose to waive the inspection, but it's a gamble.

Make an Offer and Go Under Contract

Once the home buyer finds the perfect property, they submit an offer with their real estate agent’s help. The contract details important elements like:

- Purchase price

- Closing cost negotiations, like asking the seller to pay a portion

- Contingencies (home inspection, financing, appraisal)

- Earnest money deposit

Underwriting Procedures

After the contract is accepted, the loan enters underwriting. The lender reviews all financial details to ensure the borrower meets requirements. The buyer, agent, and lender will discuss financial details again and examine the closing documents, including the Closing Disclosure. It breaks down the final closing costs and compares them to earlier estimates.

At the same time, the VA appraiser completes the home appraisal to confirm the home’s value and verify that it meets VA property standards. If issues come up, the buyer, seller, and agents may negotiate repairs or adjust the price.

Close on the Home

During closing, the homebuyer reviews all final documents. Before closing, a last walk-through ensures the home is in the agreed-upon condition. Once everything is complete, the new owner receives the keys at settlement.

How Long Does the VA Loan Process Take?

A common concern for home buyers is the timing of loan processing. For military members, PCS orders make home buying challenging when a stable address is needed for household goods delivery. While each situation varies, the VA loan process typically takes around 30 days in ideal conditions, but it's more commonly 50–55 days to close.

Despite widely circulated myths, VA loans are not significantly slower than conventional loans when handled by an experienced lender and real estate agent. Both can advocate for the buyer by sharing helpful VA loan facts with an anxious seller who's concerned about processing time.

Factors that affect the timeline include:

- Speed of pre-approval

- Appraisal scheduling

- Required repairs

- Responsiveness of the buyer and seller

- Final underwriting conditions

The VA home loan remains one of the most valuable benefits available. With advantages like no down payment, competitive VA loan interest rates, and flexible requirements, it provides a clear path to homeownership. Working with experienced lenders and real estate professionals who understand VA loans ensures the process runs smoothly and maximizes the benefits earned through military service.

By Dawn M. Smith

back to top