Photo by fizkes from Getty Images via Canva

In this article:

Military homebuyers and sellers operate within a system that differs significantly from civilian real estate transactions. Their decisions are often driven by official military orders, strict reporting timelines, and housing allowances tied to duty station location.

Working with service members requires more than understanding the local market, pricing strategy, or inventory levels. It requires understanding the military relocation system.

A Permanent Change of Station (PCS move) or military move can occur at any time of year, although late spring through summer remains the most active season. Military families may relocate every two to four years over the course of a career.

Unique Characteristics of Military Homebuyers and Sellers

A home purchase isn’t always a long-term decision for military families. While it may be their dream home they return to one day, it might serve as a short-term residence or a potential rental property.

Service members often make real estate decisions under compressed timelines, sometimes before official orders are finalized. As mortgage rates, inventory levels, and affordability vary widely by region, military families are balancing both the realities of a PCS and the need to find a home.

Most military families begin housing research well before moving dates. That means agents are frequently working with clients remotely, coordinating digital documentation, and helping families make major financial decisions under time constraints. A real estate agent who understands military relocation processes, VA loan utilization, and current housing trends can become a stabilizing force during a major life transition.

All of these unique characteristics can make for some challenges, but it also means that military clients are usually motivated buyers and sellers. They also tend to be:

- Experienced movers

- Organized

- Prepared with necessary paperwork

- Loyal—military families can be a great source of referrals

- On a strict budget

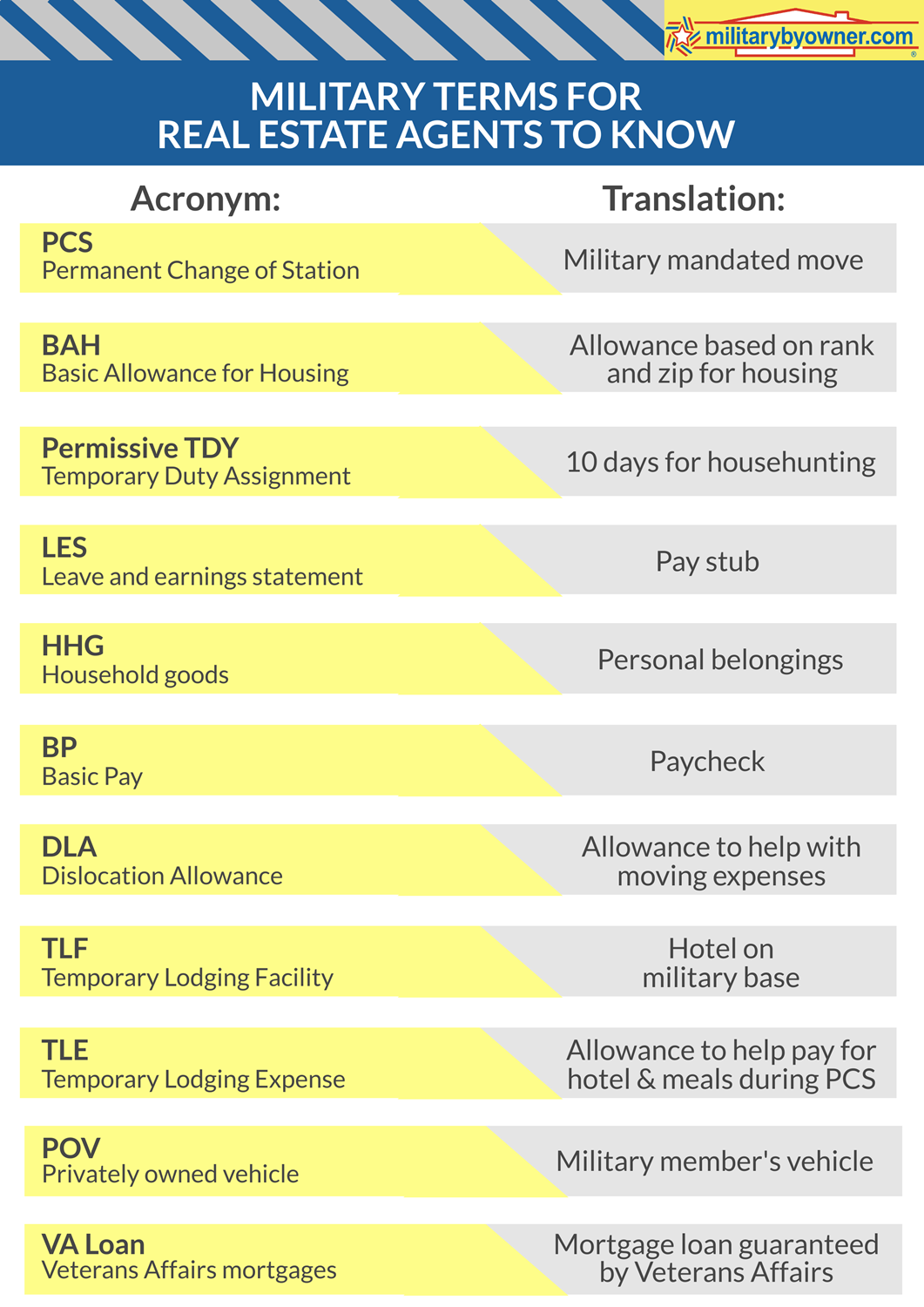

Military Terms to Know for PCS Moves

The military is fond of acronyms, and it may seem like military members and families are speaking a foreign language. With its specialized terms, the military is not unlike the real estate world. Working effectively with military clients begins with understanding the terminology that shapes their decisions.

Following is a list of military terms that apply to military relocation (PCS moves).

The VA Home Loan

The VA loan remains one of the most valuable benefits available to eligible service members and veterans. Millions have benefited from the favorable terms of the VA loan, and the program remains popular as it removes many barriers that typical buyers face, especially first-time homebuyers.

A VA Loan is backed by the U.S. Department of Veterans Affairs, which guarantees a portion of the mortgage issued by an approved lender.

This guarantee allows lenders to offer favorable terms, including:

- No required down payment in most cases

- No private mortgage insurance (PMI)

- Competitive interest rates

- Limits on certain closing costs

VA Loan Limits and Entitlement

As of 2026, veterans with full VA entitlement are not subject to a maximum loan amount and may purchase a home of any price with no down payment, provided they meet lender requirements. The loan amount must align with the home’s appraised value or purchase price, whichever is lower.

For borrowers with partial entitlement, the VA uses the Federal Housing Finance Agency’s conforming loan limits to calculate how much can be financed without a down payment. See VA.gov for the latest guidance.

The VA home loan benefit isn’t a one-time opportunity. Eligible buyers can reuse their VA loan multiple times throughout their lives, and in some cases may even carry more than one VA loan at the same time if they have remaining entitlement. Even borrowers who’ve experienced foreclosure or bankruptcy may still qualify for another VA loan in the future, provided they meet lender requirements and have sufficient entitlement available.

Our article, Have a VA Loan? Take a Second!, explains further details and examines the circumstances when it makes financial sense to look into another VA Loan.

VA Loan Funding Fee

Most VA borrowers pay a one-time funding fee on purchase and construction loans. Currently, the funding fee is 2.15% of the loan amount for first-time users with no down payment and 3.30% for subsequent users with no down payment.

Making a down payment of 5% reduces the funding fee to 1.50%, and a down payment of 10% or more reduces it further to 1.25%, whether it’s the borrower’s first use or not. Eligible borrowers, such as those receiving VA disability compensation or eligible surviving spouses, are exempt from the funding fee.

Learn more at VA.gov.

Occupancy and Property Requirements

VA loans are intended for the purchase of a primary residence located within the United States or its territories. They can’t be used for vacation homes or purely investment properties.

Eligible property types generally include single-family homes, certain condominiums in VA-approved developments, modular homes, and multi-unit properties of up to four units, provided the borrower occupies one of the units.

Properties must meet the VA’s Minimum Property Requirements, which ensure the home is safe, structurally sound, and sanitary. While minor repairs may be addressed prior to closing, homes requiring significant rehabilitation typically don’t qualify under standard VA financing unless structured through a VA renovation loan.

The VA Appraisal

Real estate agents should have an understanding of the VA requirements that affect loan approval, including the VA’s Minimum Property Requirements (MPRs).

A VA appraisal is required before a loan can be finalized. The appraiser’s role is to determine both the fair market value of the property and whether it meets VA safety and habitability standards. While some determinations require professional judgment, many MPR standards are clearly defined.

To meet VA Minimum Property Requirements, the property must:

- Be residential in nature and intended for owner occupancy

- Provide adequate space for living, sleeping, cooking, and sanitary facilities

- Have safe and functional electrical, plumbing, and heating systems

- Demonstrate sufficient remaining economic life

- Provide safe and adequate access from a public or private street

Appraisers also evaluate roof condition, structural integrity, and potential safety hazards. For homes built before 1978, peeling or chipping paint may require correction due to lead-based paint concerns.

Understanding these requirements helps agents prepare sellers and avoid delays during the appraisal process.

Learn more about the VA’s minimum property requirements.

What to Know About Military Homebuyers

Military homebuyers want many of the same things as civilian buyers, including strong school options, space for their families, and convenient access to everyday amenities. But it’s important to also understand some differences.

Installation Proximity and Community Factors

Military relocation causes these buyers to evaluate homes through a slightly different lens.

Commute time to the installation is an important factor as base traffic can significantly impact daily schedules. Proximity to childcare options, school district stability, neighborhood safety, medical facilities, and community resources can also be important factors.

While agents can’t provide guidance on neighborhood safety or school quality due to Fair Housing regulations, understanding that buyers may prioritize these concerns allows you to direct them toward appropriate resources such as GreatSchools.org, State Department of Education websites, NeighborhoodScout, local PD crime statistics, and so on.

Buying with Resale in Mind

Because many service members relocate every few years, resale or rental potential can significantly influence their decision. Location stability and long-term market strength often matter as much as interior features.

Remote Transactions and Power of Attorney

For married couples, the home-buying process may not always involve both spouses in person. A deployed or traveling service member may grant Power of Attorney to a spouse, or documents may be managed remotely.

Agents should be comfortable coordinating digital paperwork, managing inspections, and conducting detailed virtual walkthroughs when buyers can’t be there in person.

Communication and Client Experience

Military clients may need communication outside of traditional business hours due to training schedules or time zone differences, requiring flexibility and understanding.

Many military homebuyers are allotted one househunting trip, typically lasting only one week. Given this condensed timeline, it's vital for the agent to plan and coordinate several home viewings in advance, sometimes requiring long, intensive days to ensure the clients can make an informed decision before their trip ends.

Virginia Realtor Lori Ann Coyne notes,

“I love working with military families. I find them to be decisive, and they move quickly without drama. I am a military wife, so I treat them like family and make them the most important client that I have, because I know what they are going through. The next move they make should feel like an adventure, not a chore.”

Understanding BAH

Basic Allowance for Housing (BAH) is central to military housing conversations. BAH is an allowance given to military members who live off base and varies by location and rank. Some service members will also receive a COLA (Cost of Living Adjustment) for higher cost-of-living areas.

The Defense Travel Management Office calculates BAH annually based on local rental market data, pay grade, and dependency status.

While BAH is designed to offset housing costs, it doesn’t guarantee that a mortgage payment will match the allowance amount. In higher-cost markets, families may need to supplement BAH with additional income. In other areas, BAH can provide flexibility.

Agents should encourage buyers to evaluate total monthly housing costs, including:

- Property taxes

- Homeowners insurance

- HOA fees

- Utilities

- Ongoing maintenance

This BAH calculator is a great tool for homebuyers and renters to help determine their budget when purchasing a home.

Recap of Key Points for Agents Working with Military Homebuyers

- Expect accelerated timelines driven by PCS orders.

- Understand how VA financing and BAH influence purchasing decisions.

- Be prepared for remote coordination, including virtual showings and electronic signatures.

- Recognize that resale or rental potential may carry greater weight in their decision due to future relocations.

- Military buyers often have only a one-week house-hunting trip, so agents may need to plan tightly coordinated, back-to-back home viewings to help them make an informed decision quickly.

- Become well-versed on the details of using the VA Home Loan benefit (learn more about this below). Remember that both active-duty members and veterans can use the VA loan.

back to top

What to Know About Military Home Sellers

Mandated Timelines and Strategic Planning

Military home sellers rarely have the flexibility to wait for the “ideal” listing season. Military move orders dictate timelines, and agents must adapt their strategies accordingly.

Anticipate the possibility of a remote closing. Sellers may sign documents electronically or coordinate across time zones.

Evaluating the Sell vs. Rent Decision

When facing a military move, many military homeowners face a critical question: sell the property or retain it as a rental?

In a strong seller’s market, it can make sense for the military member to sell their home. In other cases, keeping the home as an investment property and renting it out may be the best option.

However, becoming a landlord, particularly from another state or overseas, means the military member will need to make some careful decisions. They’ll have to weigh whether they have the time and financial reserves to handle maintenance, comply with landlord-tenant laws, or if they should hire a property manager.

Provide balanced guidance, rather than assuming one path is preferable, to help clients make informed decisions. See tips on the selling or renting decision for service members in the post, Should I Sell My Home or Rent It Out?

Working with VA Buyers

If the buyer is using VA financing, it’s important to understand the VA appraisal process and the Minimum Property Requirements outlined above. Agents should be prepared to discuss potential repair requests identified during the appraisal and also explain that certain closing and processing fees aren’t considered allowable under VA guidelines and can’t be charged to the buyer.

Common non-allowable fees under VA guidelines include real estate commissions, lender attorney fees, and certain processing and administrative fees. Termite inspections may be also considered non-allowable in some states. in most states. These costs are typically covered by the lender or the seller.

Military home sellers who decide to use an agent’s services may be looking for a REALTOR® who’s earned the certification as a Military Relocation Professional, which means they’ve completed training to better assist military families navigate home buying and selling and are well versed in the details of VA home loans. Learn more about the MRP certification below.

Pricing and Marketing

Pricing accurately from the outset is critical when time is limited.

In addition to traditional MLS marketing, encourage sellers to list their home on the military-focused real estate site MilitaryByOwner, leverage social media, and post open house dates and virtual tours. Real estate agents can create a listing on MilitaryByOwner, too!

Tax Considerations

Military homeowners may qualify for special capital gains tax exclusions due to duty-related moves. Agents shouldn’t provide tax advice, but encourage consultation with a qualified tax professional.

Recap of Key Points for Agents Working with Military Home Sellers

- Listing timelines are often dictated by military PCS move orders rather than market seasonality.

- Understand the requirements if you’re working with a VA loan buyer.

- Remote communication or Power of Attorney may be required.

- Sell-versus-rent decisions should consider equity, market trends, and long-term plans.

- Encourage military home sellers to share their listing on as many outlets as possible, including virtual tours, social media, and sites like MilitaryByOwner.

- Pass on helpful information about what to expect at tax time, especially regarding capital gains taxes for military members.

MilitaryByOwner is here to help! Our free Guide to Selling Your Home is an invaluable tool for military home sellers.

The Military Relocation Professional Certification

A REALTOR® in good standing with the National Association of Realtors is eligible to earn the certification of Military Relocation Professional. Military homebuyers and sellers can search a national directory of MRPs and identify a REALTOR® who genuinely understands that a military move is much different than a civilian client's move. The MRP certification is highly recommended for agents who regularly work with military clients.

How do you earn the MRP certification?

- Must be in good standing with NAR (National Association of REALTORS®).

- Complete the one-day MRP certification course.

- Submit an application, including any fees, to the NAR.

According to NAR, REALTORS® who earn the MRP certification will learn:

- Demographics of the military market

- How service members can use their monthly basic allowance for housing (BAH) payment for privatized or private-sector housing

- The processes and procedures involved in a PCS move for service members and their families

- How real estate transactions for relocating military service members are unique

- How to help service members through rent or buy/sell decision-making processes

- How eligible service members and veterans can utilize VA home loan benefits

Learn more about how a Military Relocation Professional can help with a military move.

Supporting Military Families Through a Move

Military families move under circumstances most civilians never face, and a knowledgeable real estate partner can be invaluable. By understanding the demands of PCS orders, the benefits and limitations of VA financing, and the impact on military families, agents can provide guidance that feels both practical and personal.

Want to reach the military market? Explore our business ad packages below! For more resources about military families and real estate, follow MilitaryByOwner’s blog and connect with us on social media.

By Jen McDonald

back to top