Photo by superohmo via Canva.com

What to Know About Homeowners Insurance

In this article:

Buying a home is one of the most significant milestones in life, and it's often the largest financial investment people make. For military families, this investment is accompanied by unique considerations. Between frequent military moves, deployments, extended training, and an open invitation to landlord life, insurance coverage plays a crucial role in financial security and peace of mind.

While many focus solely on purchase price, mortgage rates, Basic Housing Allowance (BAH) rates, and moving logistics, overlooking the importance of homeowners insurance can leave families vulnerable. Follow along for key insights on buying a house, first-time homeowner tips, and the role of insurance in protecting one of life’s biggest investments.

Preparing to Buy a Home

Securing a reliable insurance policy begins long before move-in day.

Credit History

Credit history, for example, has an impact not only on mortgage approval but also on the cost of insurance premiums. Families with higher credit often qualify for lower rates, adding even more weight to credit reports and the need to resolve any discrepancies before beginning the homebuying process.

Damage Reports

It’s also a good idea to investigate a property’s claims history. The Comprehensive Loss Underwriting Exchange (C.L.U.E.) or the A-PLUS™ property reports reveal whether the home has suffered previous damage.

Why does this matter? Insurers use these reports to assess risk and determine pricing. A home with a new roof installed after storm damage may be viewed more favorably than one with unresolved water damage.

Home Inspection

These reports don’t, however, replace a professional home inspection. A licensed home inspection is essential. Just as lenders and buyers want assurance that a home is sound, insurance companies look closely at an inspector’s findings. If the property has outdated electrical systems, visible foundation cracks, or evidence of plumbing issues, the insurer may raise rates or even decline coverage. Addressing these concerns early prevents potential roadblocks later.

For those learning how to buy a house, these steps set the foundation for the buying process and securing affordable homeowners' insurance. First-time homeowners benefit from slowing down and treating these tasks as part of the overall purchase journey rather than last-minute details.

Reviewing credit, gathering savings for a down payment, and getting pre-approved for a mortgage all work hand in hand with preparing for insurance. Ultimately, these factors affect not just the purchase price but the long-term costs of ownership.

Photo by RDNE Stock project from Pexels via Canva.com

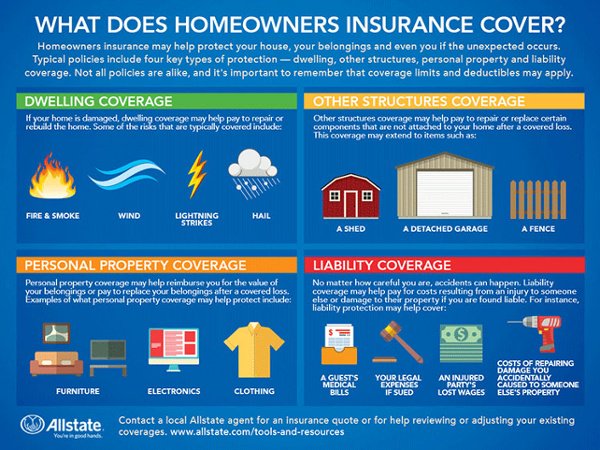

Understanding Homeowners Insurance Coverage Options

After securing the home, the next step is selecting the right type of coverage. Homeowners insurance is not one-size-fits-all; policies vary widely, as do a homeowner’s needs.

Types of Homeowners Insurance Coverage

- An Actual Cash Value (ACV) policy reimburses for damage or loss but deducts for depreciation. The payout doesn’t cover the cost of buying brand-new replacements.

- Replacement Cost Value (RCV) policies offer greater security, covering repairs and replacements at today’s prices without depreciation.

- Guaranteed or Extended Replacement Cost coverage, which pays to rebuild a home even if costs exceed the policy limits. This type of policy can be exceptionally valuable when natural disasters cause material and labor costs to spike.

How Much Coverage Do You Need?

The right coverage amount depends on more than the purchase price of the home. Insurance should reflect the cost of rebuilding, which often differs from the market value. Factors such as local construction costs, updated building codes, architectural style, and exterior features all influence the true rebuilding price.

Beyond the structure itself, coverage for personal belongings is equally important. Standard policies typically insure 50 to 70% of a home’s contents, yet this may fall short for households with extensive furniture, electronics, or collectibles. Creating an up-to-date inventory helps ensure belongings are adequately protected, should the worst happen. It’s also important to note that items such as jewelry, artwork, or antiques may require additional “floater” policies to cover their full value.

Homeowners insurance also includes:

Additional Living Expenses (ALE) provides funds for housing and food if the property becomes temporarily uninhabitable. This coverage can be critical after a fire, severe storm, or other disaster.

Liability protection is another pivotal component of a policy, covering costs if a family member or even a pet causes bodily injury or damage. Experts often recommend liability coverage between $300,000 and $500,000.

What Happens if the Home Is Vacant?

For military families, one of the most common challenges is ensuring adequate coverage when a home is left vacant. Deployments, extended training, or even temporary duty assignments, like TDYs, can cause the property to sit unoccupied for weeks or months. Unfortunately, most standard policies limit or even deny coverage once a home has been vacant for more than 30 days.

To avoid a lapse in protection, homeowners should notify their insurance company about anticipated absences. Some providers offer vacancy endorsements, vacancy clauses, or specialized coverage designed for these circumstances. Obtaining these endorsements is important because they help protect against increased risks associated with an empty home, such as vandalism, unnoticed leaks, or fire.

Insurers may also require proof that the property is being maintained. Arranging for a trusted neighbor, property manager, or family member to check the house regularly not only reassures the insurer but also helps catch potential problems early. Installing monitored security systems, smart thermostats, and water sensors can reduce risk and, in some cases, lower premiums.

The Role of Flood Insurance

One of the most common misunderstandings among homeowners is the assumption that flood damage is covered. Standard homeowners' policies don’t include flooding. And, unfortunately, it’s one of the most frequent and costly natural disasters in the country.

Families living near coasts, rivers, or designated flood zones are often required by lenders to obtain flood insurance, but even those outside high-risk areas may want to consider it. A single storm can overwhelm local drainage systems, and without coverage, homeowners are left responsible for thousands of dollars in repairs. Flood insurance is typically available through the National Flood Insurance Program as well as private insurers.

Photo by xeni4ka from Getty Images via Canva.com

Transitioning to Rental Property Coverage

Military life often comes with an open invitation to landlord life. With each set of PCS orders comes the choice to sell a home or keep it as a rental investment. For those choosing to rent, updating the insurance policy is one of the most important steps in prepping for tenants. A traditional homeowners policy is written for owner-occupied properties and does not extend coverage once tenants move in.

In these cases, a landlord policy (sometimes called a rental dwelling policy) is required. These policies generally cost more, often about 25 percent above standard homeowners insurance, because they account for the different risks associated with rental properties. In return, they provide broader protections tailored to landlords.

A landlord policy includes:

- Protection of the structure against common perils such as fire, wind, and storm damage.

- Increased liability protection in case a tenant or guest is injured on the property.

- One of the most valuable features for military families renting out a home is "loss of rental income" coverage. If the property becomes uninhabitable after a covered event, say a kitchen fire or major storm, the policy can reimburse the owner for the rental income that would have been collected during repairs. This ensures mortgage payments and other expenses tied to the property can still be met, even when tenants aren’t occupying the home.

For families managing a property from a distance, this added protection can make a significant difference. Having the right policy in place provides both financial security and peace of mind, allowing homeowners to focus on their next duty station and current cost of living rather than worrying about gaps in coverage back home.

Note: While landlord insurance covers the structure, liability, and loss of rental income, it does not protect a tenant’s personal belongings. Renters should be required, through the lease, to obtain their own renters’ insurance policy.

Why Homeowners Insurance Costs Vary

The cost of homeowners' insurance, or even realizing that coverage is difficult to obtain, surprises many military homebuyers. Premiums have risen steadily in recent years, driven by the increasing frequency and severity of natural disasters. Homes in coastal areas, flood zones, or earthquake-prone regions often face higher premiums or limited options.

Other property characteristics influence costs as well, making them more expensive to insure:

- Older homes with time period finishes or outdated electrical or plumbing systems

- Properties located in areas prone to natural disasters

- Roofs in poor condition

- Construction that does not meet current building codes

Amenities such as swimming pools or trampolines increase liability risks, often requiring higher coverage limits. In some cases, insurers may decline to offer a policy unless the homeowner makes certain upgrades or repairs first.

Reducing Policy Rates for Military Homeowners

Although homeowners’ insurance is a necessary expense, there are ways to reduce costs. Raising deductibles is one option, but it requires careful consideration and often requires a hefty emergency fund. Bundling policies, such as combining auto and home insurance with the same provider, often leads to discounted rates.

Routinely reevaluate the policy to ensure that coverage levels remain appropriate. As possessions change in value, floater policies may no longer be necessary, while new purchases might require added protection. Many insurers also offer discounts for safety improvements such as smoke detectors, security systems, or smart home technology. Asking directly about available discounts, including military-specific options, can help save money.

The Bottom Line for Military Families

Homeownership is both a privilege and a responsibility, and homeowners' insurance, though it costs money, protects that investment. For military families and first-time homeowners, the need for adequate coverage is heightened by the realities of active-duty life. Unexpected deployments, frequent relocations, and the possibility of managing a property from afar all lead to the need for a protective buffer.

Whether navigating the decision to buy or rent, preparing a home for vacancy, or transitioning into life as a landlord, insurance is the cushion that allows military families to move forward with confidence. Taking time to research providers, ask questions, and secure appropriate coverage ensures that, no matter where duty calls, the investment remains protected.

Buying a home? Get our free home buying guide below.

back to top